In this guide, we’ll break down the confirmed SDLT rules, current rates, surcharges, and possible reforms now under discussion.

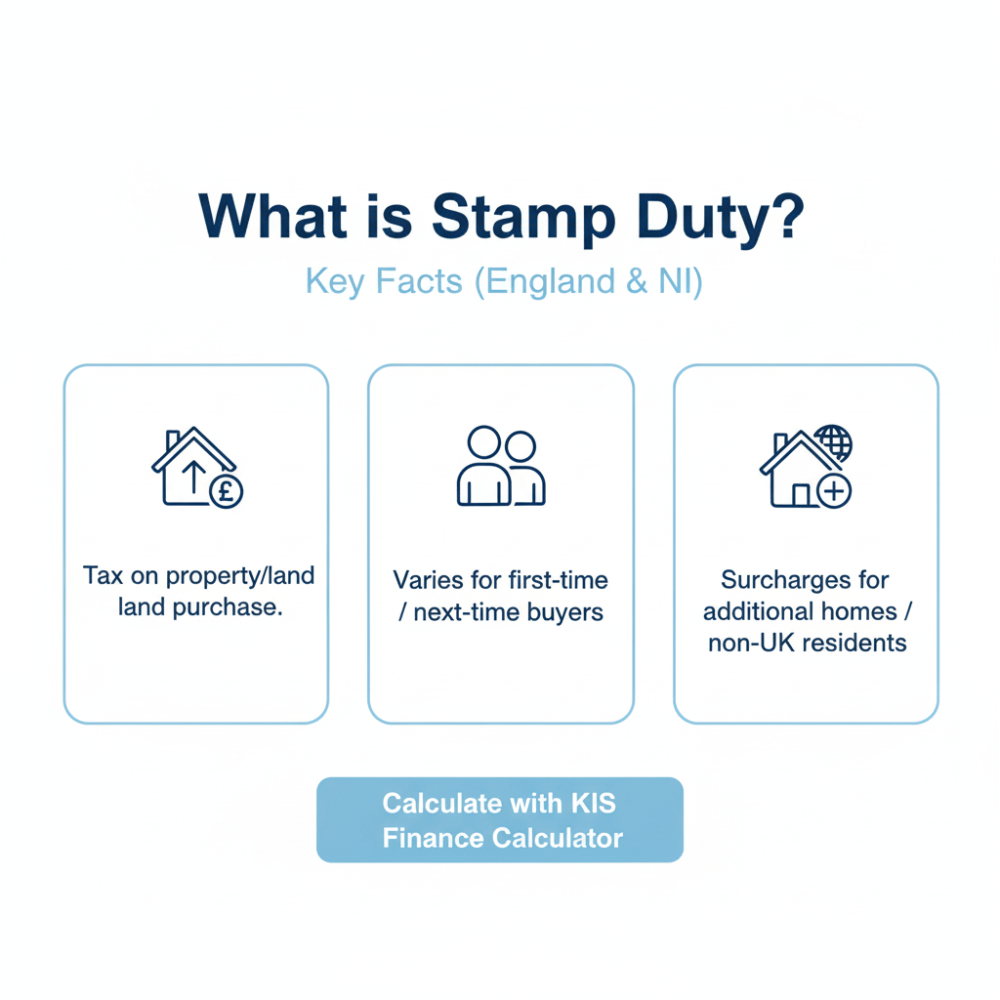

What is stamp duty?

Stamp duty land tax (SDLT) is a tax you pay when purchasing residential property or land in England and Northern Ireland. It applies to both freehold property and leasehold property, including new builds and shared ownership schemes.

Scotland and Wales operate separate systems: Land and Buildings Transaction Tax (LBTT) and Land Transaction Tax (LTT). SDLT is calculated using tiered stamp duty rates, which increase as the property price rises.

You can easily calculate your SDLT liability before completing a purchase with the KIS Finance stamp duty calculator, which is considered one of the best on the market.

So, here are the main points about stamp duty to clear the air:

- Applies to most property transactions above the nil rate threshold

- Different thresholds for first time buyers and standard buyers

- Additional properties and non-UK residents pay surcharges

Current stamp duty rules for 2026

From April 2025, the UK government announced permanent stamp duty changes that affect property transactions in England and Northern Ireland.

The nil rate threshold reverted to £125,000, while first time buyers relief applies up to £300,000 on homes with a maximum purchase price of £500,000. Anyone buying additional properties pays a 5% surcharge, and non-UK residents pay an extra 2%.

| Price Bracket (£) | Stamp Duty Rates |

| 0 – 125,000 | 0% |

| 125,001 – 250,000 | 2% |

| 250,001 – 925,000 | 5% |

| 925,001 – 1.5 million | 10% |

| Above 1.5 million | 12% |

Key points for 2026:

- Standard residential property bands apply to most buyers

- First time buyers receive relief but only within capped property values

- Investors and landlords face higher surcharges

Practical examples of SDLT in 2026

Stamp duty in 2026 is based on property price bands, with extra costs for additional properties and non-UK residents. Below are clear examples to show how the tax works.

- First time buyers, £300,000 home

- 0% on first £300,000 = £0

- Total = £0 (within first time buyers relief limit)

- Standard buyer, £400,000 home

- 0% on first £125,000 = £0

- 2% on next £125,000 = £2,500

- 5% on remaining £150,000 = £7,500

- Total = £10,000

- Additional property, £300,000 home

- Normal SDLT = £5,000

- 5% surcharge = £15,000

- Total = £20,000

- High-value home, £1,000,000

- SDLT bands apply, including 10% from £925,001 to 1.5 million

- Total = £43,750

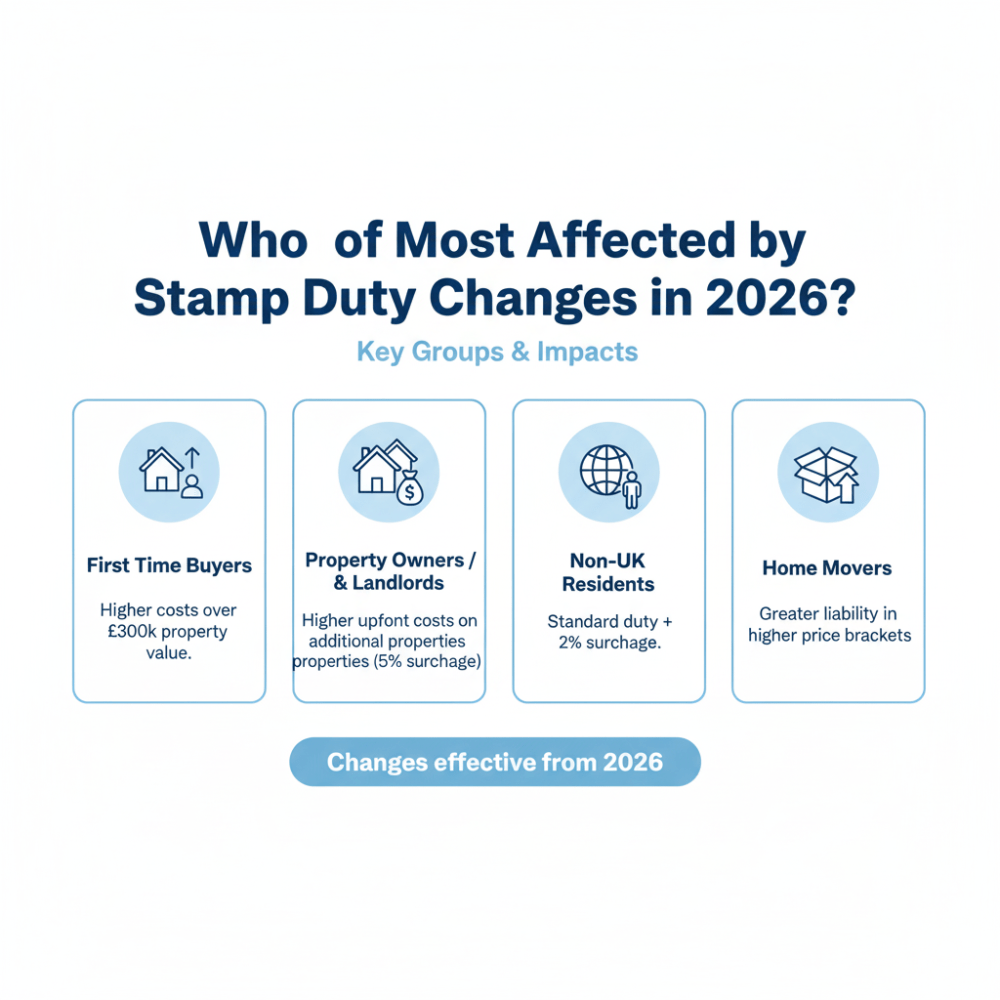

Who is most affected?

Stamp duty changes in 2026 will affect different groups of buyers in distinct ways.

The reduction of the residential nil rate threshold will increase costs for many, while surcharges will raise liabilities further.

We can define 4 key groups:

- First time buyers lose the wider relief offered between 2022–2024 and now pay more once property values exceed £300,000.

- Property owners and landlords face higher upfront costs on additional properties due to the 5% surcharge.

- Non-UK residents must pay the standard duty land tax plus a 2% surcharge.

- Home movers purchasing at higher price brackets carry greater stamp duty liability compared to previous years.

What might change in 2026?

The UK government and think tanks are discussing new property tax reforms that could replace or alter the current stamp duty system. While no changes are confirmed, several ideas are under review.

Proposals under discussion:

- Annual property tax for homes above £500,000, paid by sellers instead of buyers

- Mansion tax on high-value properties above 1.5 million

- Council tax band reform to adjust payments based on updated property values

- Replace council tax and SDLT with a new property tax model

Note that these remain speculative and are not yet law. Buyers should follow the autumn statement for updates.

Regional variations

Stamp duty land tax applies only in England and Northern Ireland. Scotland and Wales operate separate systems with their own thresholds and property tax structures. Buyers must check rules specific to the region.

| Region | Tax System | Zero-Rate Threshold | Notes |

| England & N. Ireland | SDLT | £125,000 (£300,000 for first time buyers) | Surcharges apply |

| Scotland | LBTT | £145,000 | Separate rates |

| Wales | LTT | £225,000 | Own property bands |

Practical implications for buyers and sellers

Stamp duty in 2026 increases upfront costs compared with the temporary increase in thresholds during 2022–2024.

Buyers, landlords, and non-UK residents must calculate SDLT liability carefully before completing property transactions. Sellers of high-value homes may face new property tax reforms if parliamentary proposals move forward.

Key implications:

- Buyers need to budget for higher SDLT, especially above the nil rate threshold

- First time buyers benefit only within the £300,000 limit and below the £500,000 maximum purchase price

- Property owners with additional properties pay higher surcharges

- Non-UK residents face combined surcharges and higher SDLT liability

Conclusion

Stamp duty in 2026 applies under permanent rules set in April 2025, with lower nil rate thresholds and higher costs for many property transactions.

First time buyers relief supports purchases up to £300,000, while investors and non-UK residents face added surcharges. Proposals such as an annual property tax or mansion tax remain under discussion, but no new system is confirmed.

Key takeaways:

- SDLT bands define what buyers pay across property values

- Relief applies only under strict limits for first time buyers

- Additional properties and overseas buyers carry higher SDLT liability

- Future reforms may change how property tax is collected

FAQs

1. What are the current stamp duty rates in 2026?

Stamp duty land tax (SDLT) in 2026 applies to residential property purchases in England and Northern Ireland. The nil rate threshold is £125,000 for most buyers. First time buyers benefit from a £300,000 nil rate threshold if the property value does not exceed £500,000. Standard SDLT rates are 0% on £0–125,000, 2% on £125,001–250,000, 5% on £250,001–925,000, 10% on £925,001–1.5 million, and 12% above £1.5 million.

2. Do first time buyers get any relief in 2026?

Yes. First time buyers relief applies if the home costs less than £500,000. No SDLT is paid on the first £300,000, and 5% is paid on the portion between £300,001 and £500,000. If the property exceeds £500,000, the relief does not apply and standard SDLT rates are charged.

3. How does stamp duty affect additional properties in 2026?

Purchases of additional properties such as second homes or buy-to-let investments incur a 5% surcharge on top of the standard SDLT bands. For example, a £300,000 second home attracts standard SDLT of £5,000 plus an additional surcharge of £15,000, giving a total of £20,000.

4. Are there extra charges for non-UK residents in 2026?

Yes. Non-UK residents pay the standard SDLT rates plus a 2% surcharge on residential property purchases. If the property also qualifies as an additional property, both surcharges apply, increasing total SDLT liability.

5. Could stamp duty rules change again in 2026?

The government is considering reforms such as replacing SDLT with an annual property tax for homes valued over £500,000 or introducing a mansion tax. Council tax band reform is also under discussion. These proposals remain unconfirmed and subject to future parliamentary decisions.

6. How do stamp duty rules differ across the UK?

England and Northern Ireland use SDLT. Scotland applies Land and Buildings Transaction Tax (LBTT), while Wales uses Land Transaction Tax (LTT). Each system has distinct thresholds, rates, and surcharges, so property transactions must follow the rules of the relevant jurisdiction.

7. How much SDLT would a buyer pay on a £400,000 home in 2026?

A standard buyer pays £10,000: £0 on the first £125,000, £2,500 on the next £125,000, and £7,500 on the remaining £150,000. A first time buyer would pay £5,000, as no tax is charged on the first £300,000 and 5% applies to the remaining £100,000.