Credit risk has always involved judgment, but the raw material behind that judgment has changed. Lenders no longer rely only on static files, repayment history, and broad score ranges to decide who looks safe and who needs a closer look. They now work with faster signals, wider data sets, and a much stronger expectation that risk decisions should be both accurate and explainable. That shift has made credit risk analytics far more important than its name may suggest.

Today, a credit risk API may feed fresh borrower and account data directly into underwriting, monitoring, and portfolio review workflows, but the real story is bigger than the technology itself. Credit risk analytics now helps teams spot pressure earlier, compare borrowers more intelligently, and respond to changing conditions with more precision than older models allowed. The latest trends clearly reflect that change. Better prediction still matters, but so do transparency, fairness, and the ability to keep models useful as markets and borrower behavior shift in new directions.

What Credit Risk Analytics Covers

At its most basic level, credit risk analytics is the set of methods a lender uses to measure and manage the risk that a borrower will fail to meet an obligation. That includes origination decisions, portfolio reviews, loss forecasting, limit setting, collections strategy, and stress testing. Some analytics are close to the front line. Others are built for finance, risk committees, or regulatory reporting.

The field is wider than many people expect. It is not only about saying yes or no to an application. It also helps answer harder questions. How much risk is in a certain segment? Which exposures are weakening? How much capital should be held against expected losses? Which borrowers need a closer look before the next review cycle?

That is why credit risk analytics matters far beyond underwriting teams. It shapes portfolio construction, product design, provisioning, and strategic planning. A good model can improve approvals. A good analytics framework can improve the whole credit process.

The Data Behind the Models

Traditional credit analytics still leans heavily on bureau history, repayment performance, utilization patterns, financial statements, collateral data, and sector-level performance. None of that has disappeared. These inputs remain useful because they create a long historical base and help lenders compare borrowers consistently across time.

What has changed is the mix. More institutions are combining classic credit data with account behavior, permissioned cash flow signals, internal transaction history, customer-level servicing data, and market context that updates faster than old reporting cycles. The model is no longer expected to look only backward. It is expected to say something useful about present conditions and near-term pressure.

That shift matters because many borrowers do not fit neatly into older credit categories. Some have limited bureau depth. Others have stable operations that are not obvious from static reports. Better data does not solve every problem, but it gives the analytics team more room to see financial behavior as it actually happens.

How Lenders Actually Use It

In practice, credit risk analytics does several jobs at once. At origination, it supports approval, pricing, and limit decisions. After booking, it helps monitor deterioration, identify early warning signs, and guide collection or account management strategies. At the portfolio level, it helps lenders compare segments, concentration risk, vintage quality, and expected loss trends.

This is also where the discipline gap shows up. Some firms have strong models and weak workflows. Others have plenty of data but poor translation between analytics and decision-making. A score, on its own, is not a risk framework. It becomes one only when it connects clearly to policy, thresholds, escalation, and human review.

The better institutions treat analytics as an operating tool, not a technical ornament. That means results are visible, challengeable, and tied to real decisions. It also means models are reviewed when business conditions shift, not only when validation schedules say it is time.

AI and Machine Learning Are Moving Further in, but With More Scrutiny

One of the clearest trends is the deeper use of AI and machine learning in credit analytics. Lenders want models that can handle larger datasets, detect subtler patterns, and improve segmentation beyond what traditional scorecards can achieve on their own. That push is real, and it is not slowing down.

At the same time, scrutiny has increased. Regulators and central banks have been clear that model sophistication does not reduce the need for explainability, risk management, and oversight. In fact, more complex models often create more pressure to show how decisions are reached, how performance is tested, and how model risk is managed.

That has changed the conversation. The industry is no longer asking only, “Can machine learning predict better?” It is also asking, “Can we explain it, govern it, monitor it, and defend it when a borrower or supervisor asks harder questions?”

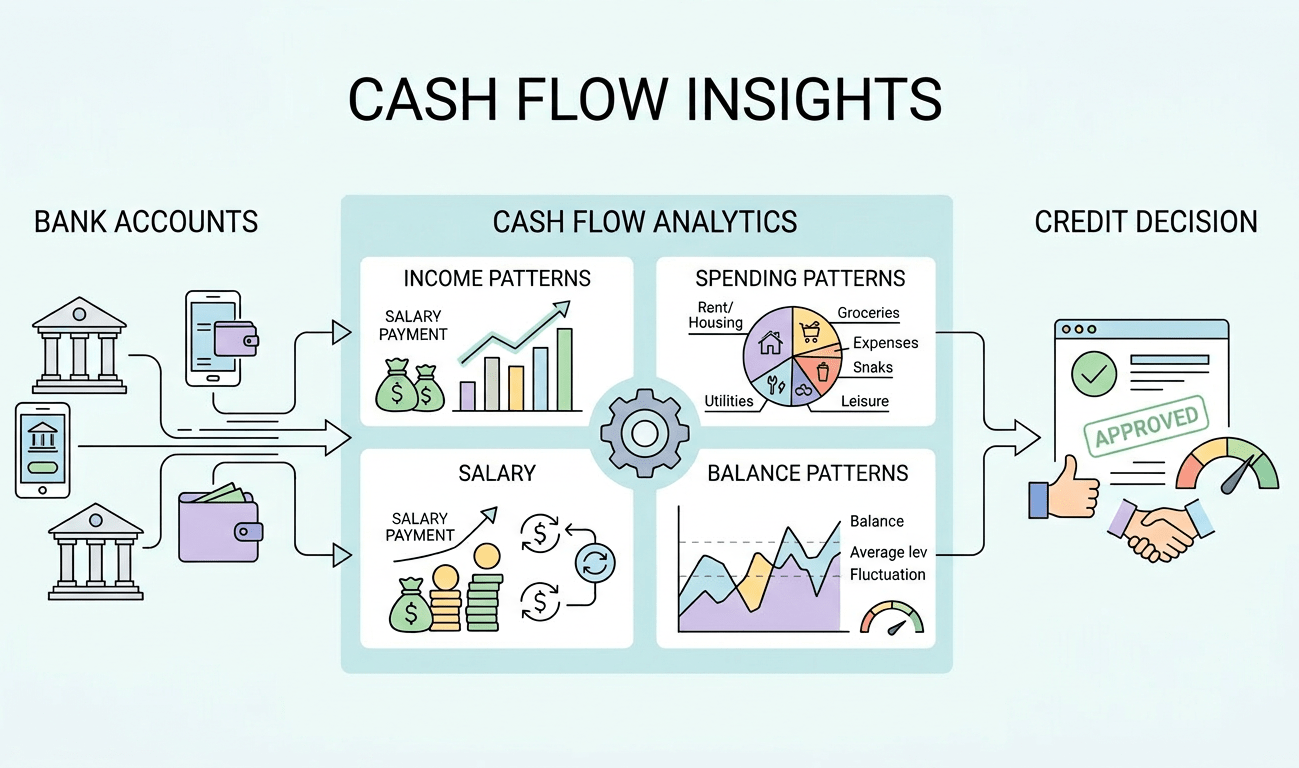

Cash Flow and Open Finance Data Are Gaining Ground

Another major shift is the rise of cash-flow and open-finance data in credit assessment. Lenders are increasingly using permissioned account information to study income stability, spending pressure, seasonal patterns, and balance behavior. This is especially useful where traditional files are thin, outdated, or incomplete.

The practical value is easy to see. A borrower may look weak in a classic score model and still show healthy account discipline. Another may present acceptable headline numbers while transaction-level behavior points to strain. Cash flow data helps narrow that gap between surface information and operating reality.

This trend is also widening access in a more disciplined way. Instead of lowering standards, lenders can use richer signals to make finer distinctions. That can improve confidence in approvals, sharpen pricing, and give smaller businesses or newer borrowers a fairer read than a bureau file alone.

Early Warning Monitoring Is Becoming More Continuous

Credit analytics used to lean more heavily on periodic reviews. That rhythm still exists, but it is being supplemented by more continuous monitoring. Risk teams want to see deterioration earlier, not after a quarterly review package lands or arrears have already appeared.

That is pushing lenders toward stronger early warning systems. Key risk indicators, account behavior changes, payment stress signals, sector-specific pressure, and internal servicing data are being used more actively to flag exposures that deserve attention sooner. In some firms, the real gain is not one dramatic predictive breakthrough. It is the ability to move faster once a pattern starts to shift.

This trend also changes the workload inside risk functions. Monitoring is becoming more data-intensive and more operational at the same time. The teams that do it well are building cleaner pipelines, more usable alerts, and better handoffs between analytics, credit officers, and portfolio managers.

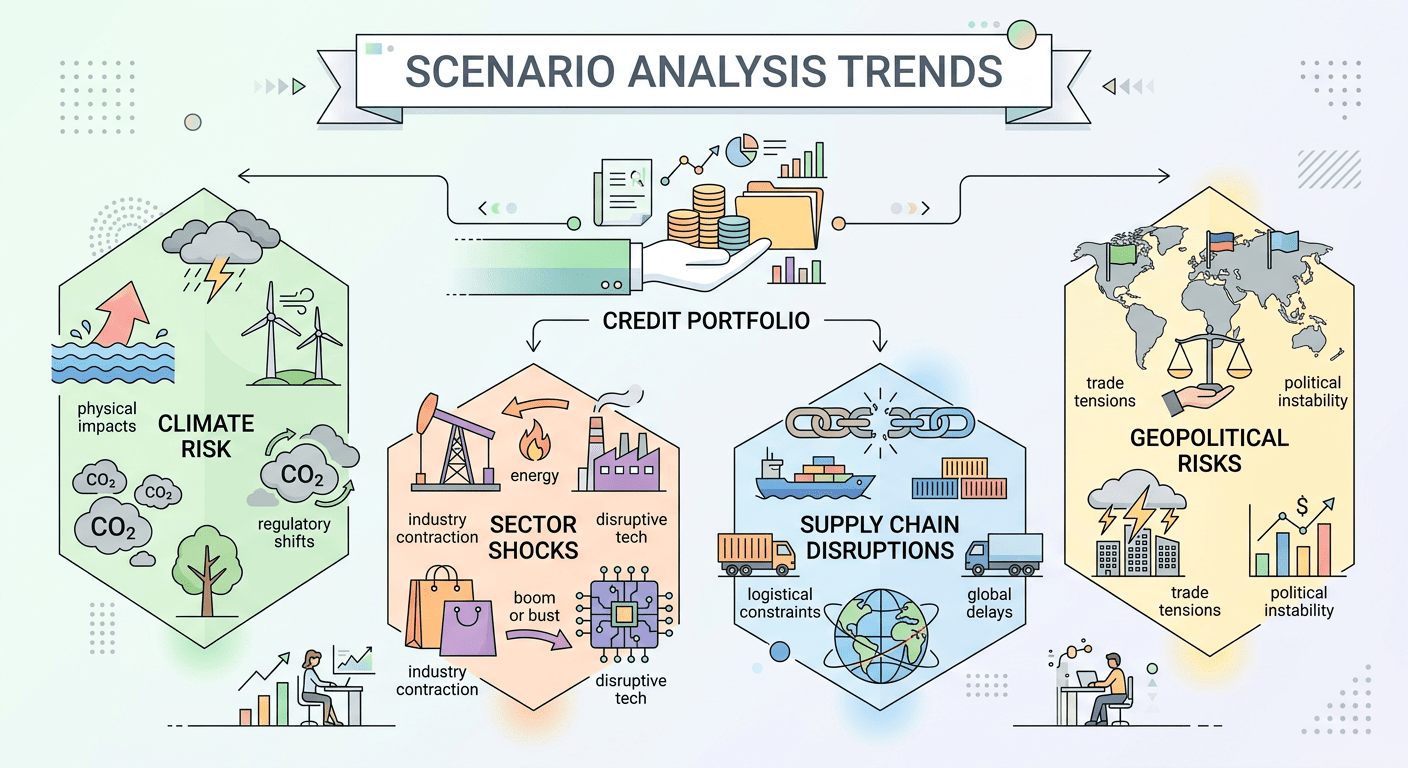

Scenario Analysis Is Expanding Beyond the Usual Credit Cycle

Stress testing is not new, but the inputs are changing. Credit teams are now expected to think more seriously about climate exposure, sector transitions, supply chain disruptions, tariff pressure, and second-order effects that do not appear clearly in standard historical default tables. That has made scenario analysis more important and more complicated.

Climate and nature risk is one part of this shift. Supervisors have been pushing banks to move from broad statements to actual monitoring practices across relevant exposures and geographies. That is a meaningful change. It asks credit analytics to connect portfolio quality with external physical and transition risks in a way that many institutions were not built to do a few years ago.

The same broader logic applies to macro and sector shocks. Credit analytics is now expected to look beyond “base, mild stress, severe stress” templates and provide more practical insight into portfolio vulnerability when conditions shift unevenly across industries or regions.

Governance, Fairness, and Human Judgment Matter More Than Ever

The final trend is not really technical, even though technology helped create it. As credit analytics becomes more advanced, the governance burden gets heavier. Institutions need clearer validation, stronger documentation, better data lineage, and more confidence that adverse decisions can be explained accurately. There is no real appetite, from supervisors or from borrowers, for a credit process that cannot account for itself.

Fair lending pressure is part of this, too. If a model uses broader data and more complex logic, the institution still has to explain why a customer was declined or repriced. That means fairness testing, reason codes, and governance are no longer side issues. They are close to the center of the analytics conversation.

Human judgment remains important for the same reason. Good credit risk analytics should sharpen decisions, not replace thinking. The strongest risk functions are not choosing between people and technology. They are building a framework where better models, cleaner data, and experienced judgment all work in the same direction.